Last week’s economic landscape was dramatically reshaped by President Trump’s announcement of sweeping tariff policies on what he declared “Liberation Day.” His announcement triggered a historic sell-off in the stock market. Equities experienced their worst single-day decline since March 2020. They plummeted to their lowest levels in over 11 months as investors grappled with the potential implications of the new trade barriers.

This market turmoil unfolded against a backdrop of seemingly resilient economic data. That included a robust March employment report that significantly exceeded expectations. However, the strength in the labor market is now viewed with caution. That is the looming impact of tariffs raises serious questions about future economic growth and business activity. Other indicators like the JOLTS report showed some softening in job openings. And both the services and manufacturing sectors presented a mixed picture of expansion and contraction. But the dominant narrative last week was undoubtedly the shockwaves sent through the market by the newly announced tariff policies.

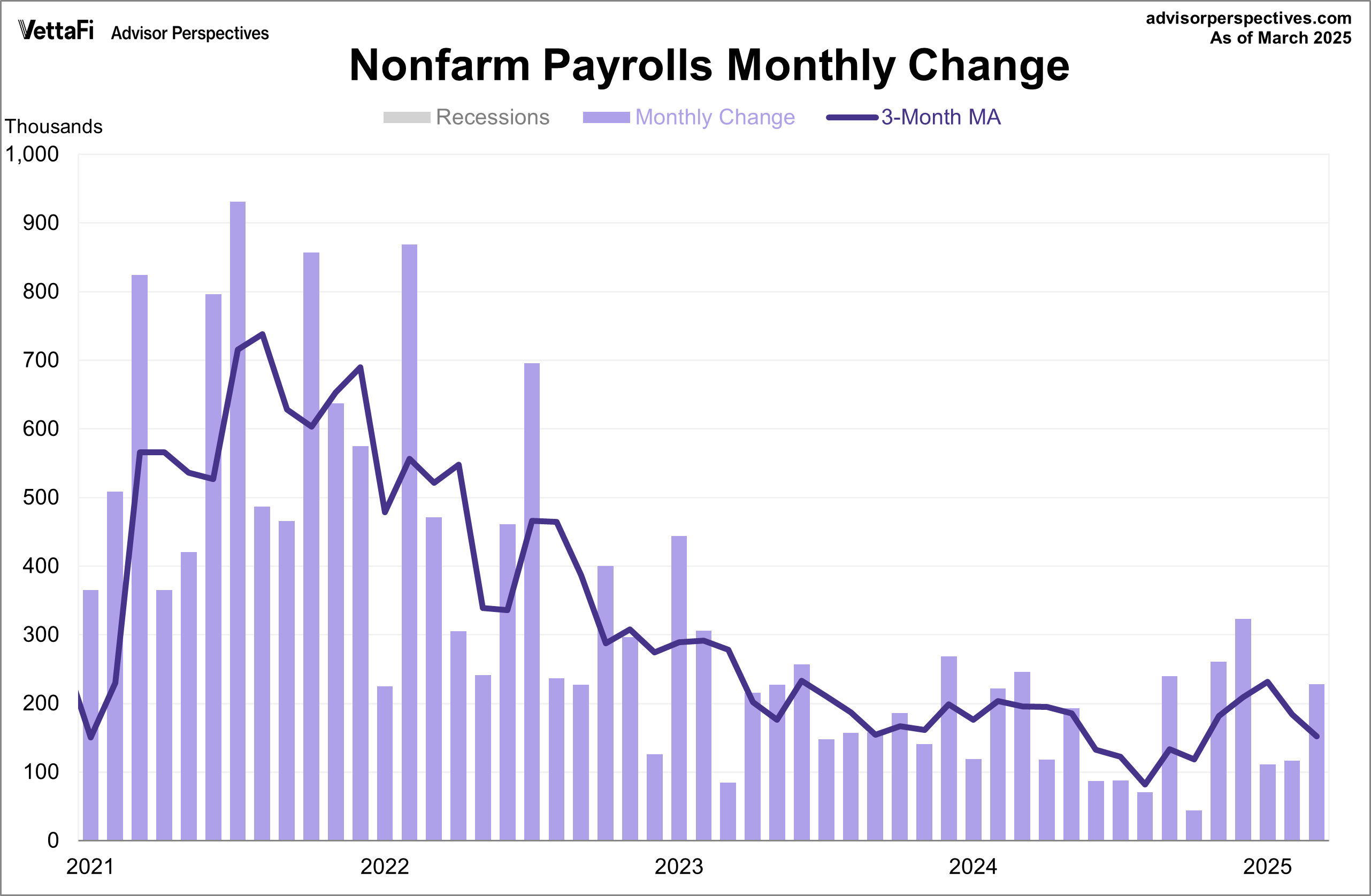

Employment Report

The U.S. labor market remained strong in March, though the sweeping tariffs announced last week have raised questions about how much longer that strength can last. The latest employment report showed that 228,000 jobs were added last month, exceeding the expected 137,000 addition. This is the largest job growth of 2025 so far. Meanwhile, the unemployment rate unexpectedly inched up to 4.2% from 4.1% in February, reaching its highest level in four months but remaining near historically low levels. Wage growth also remained stable, with average hourly earnings increasing by 0.3% from the previous month, as expected. Annually, wages grew by 3.8%, a slowdown from 4.0% in February and lower than the projected 3.9% growth.

The labor market has shown resilience in the face of elevated rates over the past few years, with 51 consecutive months of job growth. While March’s data supports this narrative, concerns have drastically increased about a potential downturn due to President Trump’s economic and tariff policies. Many are viewing the latest report as a “rearview mirror” look at the economy.

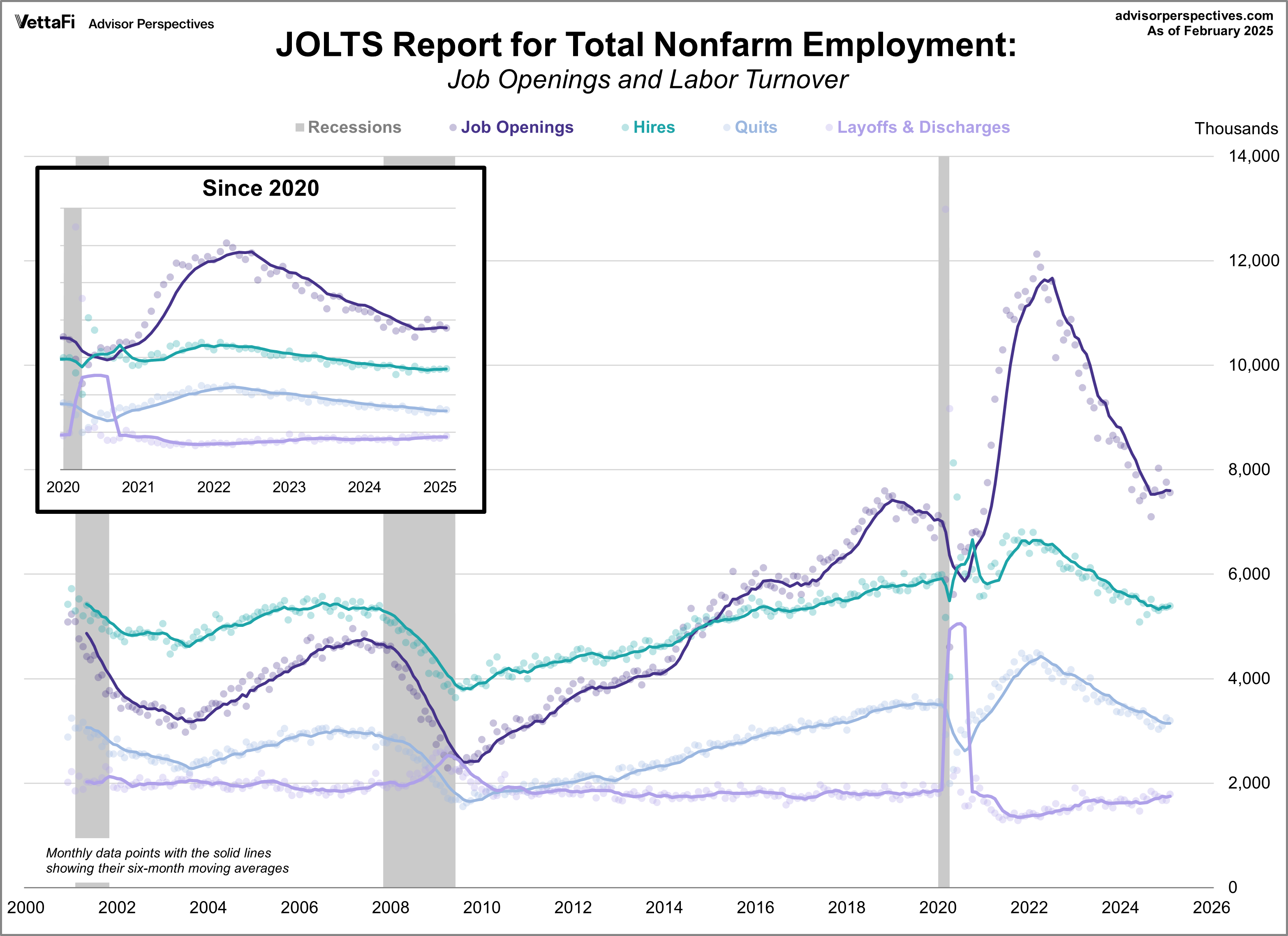

Job Openings & Labor Turnover Summary (JOLTS)

Job openings fell more than expected in February, but overall, turnover held steady. The latest JOLTS report indicated job openings fell by 194,000 to 7.568 million, falling short of the predicted 7.690 million. Although openings remain above prepandemic levels, they have steadily declined over the past 2.5 years and currently sit at 4.5 million below their 2022 peak.

The report also showed that hires and layoffs saw slight increases, while quits declined. However, the percentage of hires, layoffs, and quits of total employment were all unchanged in February. The hiring rate stayed close to its lowest point in the past 10 years, at 3.4%. Quits — which indicate worker confidence — remained at 2.0%, and layoffs stayed at 1.1%.

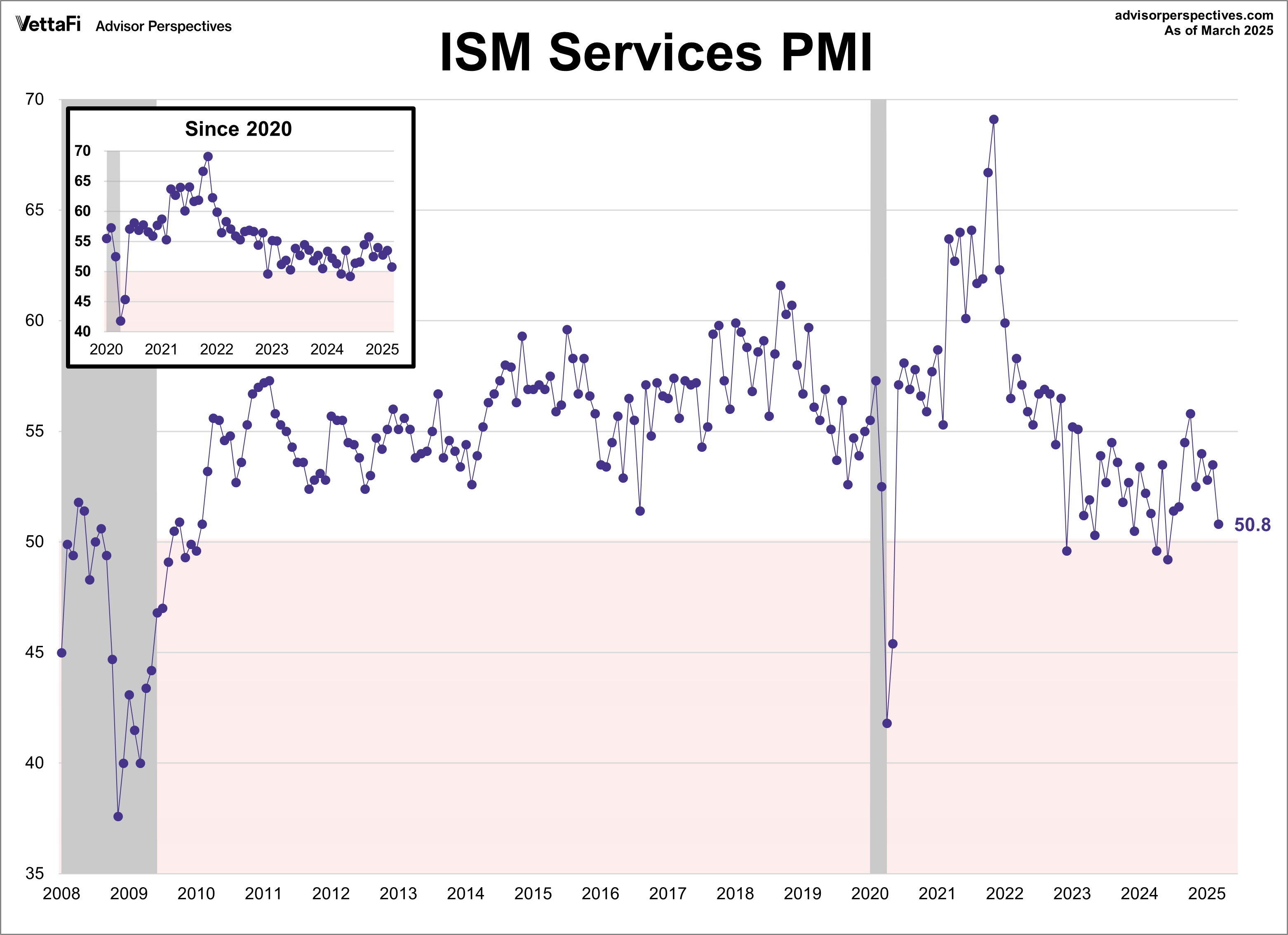

ISM Services

The U.S. services sector continued to expand in March, although at its slowest pace since June. The ISM Services PM dropped more than expected — to 50.8 from 53.5 in February. The index was expected to inch down to 53.5. Three of the four components that factor directly into the PMI were in expansion territory last month, with Employment as the sole subindex in contraction. Additionally, three of the components fell from the previous month, with Business Activity as the sole subindex seeing an increase. The services sector has now expanded in 25 of the last 27 months, dating back to January 2023. However, there were mixed comments from respondents regarding future activity, with some expecting declines and others with good outlooks.

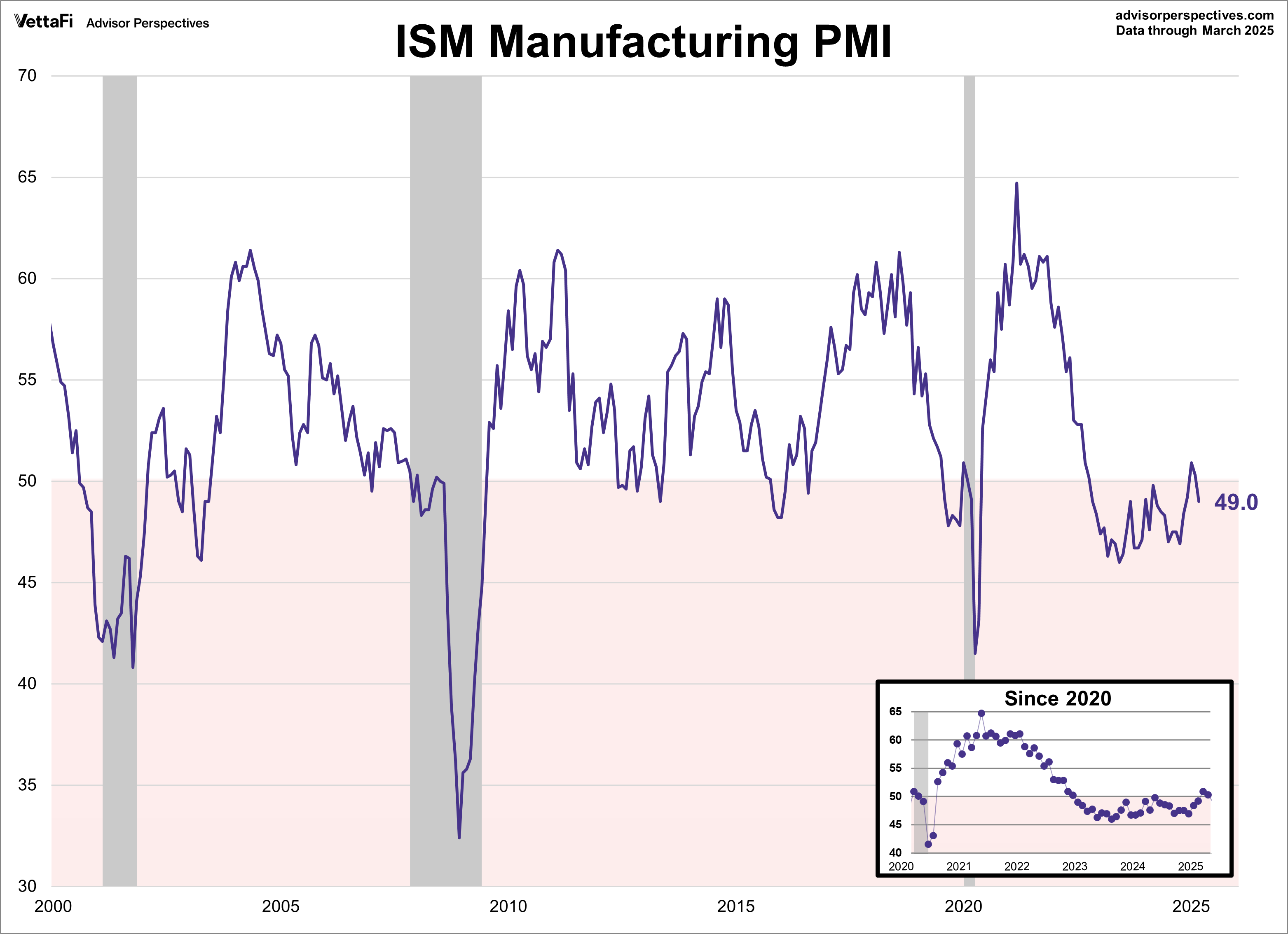

ISM Manufacturing

U.S. manufacturing activity contracted last month after marginal expansion in February. The ISM Manufacturing PMI dropped to 49.0 in March from 50.3 in February, falling short of the 49.5 forecast. Several subcomponents hinted at inflationary pressures on the rise because of tariffs. The New Orders and Employment components fell further into contraction territory, while price growth continued to accelerate. The manufacturing sector has now contracted for 27 of the past 29 months, with respondents reporting significant concerns regarding tariffs and their overall impact for future growth.

ETFs associated with industrials and manufacturing include: First Trust Industrials/Producer Durables AlphaDEX Fund (FXR), Industrial Select Sector SPDR Fund (XLI), Vanguard Industrials ETF (VIS), and iShares U.S. Industrials ETF (IYJ).

Market Reactions

The S&P 500 began the week with three straight daily gains, but then “Liberation Day” led the index to its two worst days since March 2020. The index ended the week with a 9.1% loss and has reentered correction territory. As a result, the SPDR S&P 500 ETF Trust (SPY) fell 9.0% last week. Meanwhile, the S&P Equal Weight Index was down 8.6% from the previous week, and the Invesco S&P 500 Equal Weight ETF (RSP) fell 8.5%.

The yield on the 10-year note ended April 4, 2025 at 4.01%, while the two-year note ended at 3.68%. These are the lowest levels for each respective note since October.

Rate cut expectations shifted yet again last week. The CME FedWatch Tool currently shows four 25 basis point cuts for 2025, coming at the June, July, September, and December meetings. One additional 25 basis point cut is expected in 2026.

Economic Data in the Week Ahead

The upcoming week will feature some of the most closely watched economic data. The Bureau of Labor Statistics will release the Consumer Price Index (CPI) for March on Thursday and the Producer Price Index (PPI) on Friday. These reports will provide the latest inflation update, which continues to be a major area of focus for consumers, businesses, investors, and policymakers. Also on Friday, the University of Michigan will release its preliminary consumer sentiment report for April, which has recently plummeted to multiyear lows on tariff and inflation concerns.

For more news, information, and strategy, visit the Innovative ETFs Channel.

Financial Market Newsflash

No financial news published today. Check back later.