Central Garden & Pet Company (CENT – Free Report) stands out as a resilient player with a diversified portfolio, spanning pet consumables, garden supplies and live goods. CENT has consistently demonstrated its ability to adapt, innovate and drive value, despite shifting market dynamics.

Backed by a clear strategic vision, disciplined cost management and a growing digital footprint, the company is well-positioned for sustainable, long-term growth. Here is a closer look at the key factors supporting the company’s upward momentum in fiscal 2025 and beyond.

Central Garden & Pet’s Visionary Growth Strategy in Action

Central Garden & Pet is strategically positioning itself as a dominant player in the U.S. pet and lawn and garden supplies market. The company continues to benefit from distinctive packaging, effective point-of-sale displays, robust logistics and exceptional customer service. A cornerstone of its growth strategy, Central-to-Home, is gaining traction through enhanced digital capabilities, an optimized supply chain and elevated marketing efforts.

Central Garden & Pet is investing in a robust pipeline of new products across its pet and garden segments, with launches scheduled for fiscal 2025 and beyond. The company is focused on innovation to meet evolving consumer preferences, including high-quality pet consumables and sustainable garden solutions.

CENT’s Cost and Simplicity Program

CENT’s multi-year Cost and Simplicity program is proving effective in driving operational efficiency. From Stock Keeping Unit rationalization to facility consolidations and enhanced tech integration, these efforts are reducing complexity and improving productivity. A key milestone is the opening of its Covington, GA, distribution center, which has streamlined operations by replacing seven older facilities.

As a result, adjusted gross margin expanded 160 basis points to 29.8% in the first quarter of fiscal 2025. Moreover, SG&A expenses fell 2% year over year and operating margins jumped 300 bps to 4.3%, reflecting disciplined cost management.

CENT’s E-Commerce and Digital Strength

CENT’s investments in digital infrastructure are paying off, particularly in the Pet segment, where in the first quarter of fiscal 2025 sales rose 4% to $427 million, buoyed by strong demand in dog and cat categories. E-commerce now represents 28% of pet segment revenues, growing at a healthy 6% year over year. Enhanced digital capabilities, retail media strategies and data analytics are reinforcing the company’s online presence.

The Garden segment registered double-digit e-commerce growth, supported by improved content and media strategies. In the fiscal first quarter, Garden revenues grew 2% to $229 million, fueled by robust bird feed and fertilizer sales. As weather normalizes and seasonal demand picks up, this segment is well-positioned for continued strength.

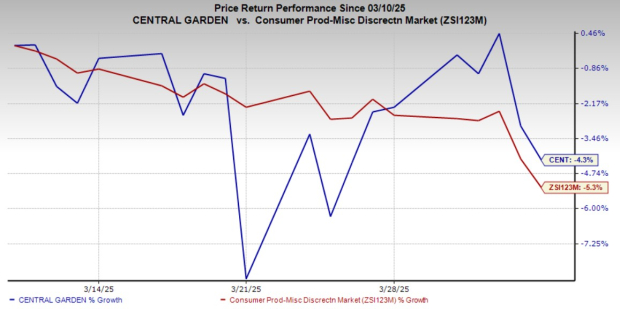

CENT Stock’s Performance

Although shares of CENT have dipped 4.3% in the past month, it has outperformed the industry’s decline of 5.3%. The recent weakness in CENT stock’s performance can partly be linked to investor concerns over tariffs.

CENT Stock Past Month Performance

Image Source: Zacks Investment Research

CENT is currently trading at a discount to its historical and industry benchmarks. Central Garden & Pet’s forward 12-month price-to-sales multiple is 0.71X, down from its median level of 0.78X in the past year and the industry’s multiple of 3.09X. This implies that relative to its earnings potential, CENT stock might still be undervalued. For investors, this presents an attractive opportunity, which is further underscored by CENT’s current Value Score of A.

Image Source: Zacks Investment Research

Final Words on CENT

Despite near-term headwinds such as tariffs and macroeconomic uncertainty, Central Garden & Pet’s strategic focus on innovation, cost optimization and digital expansion, supported by impactful initiatives, like the Cost and Simplicity program and Central-to-Home strategy, positions it for sustained long-term growth. These initiatives are not only enhancing operational efficiency but also strengthening this Zacks Rank #1 (Strong Buy) company’s brand equity and competitive position.

Other Stocks to Consider

United Natural Foods, Inc. (UNFI – Free Report) distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. It currently carries a Zacks Rank of 2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for United Natural Foods’ current financial-year sales and earnings implies growth of 1.9% and 485.7%, respectively, from the year-ago figures. UNFI delivered a trailing four-quarter earnings surprise of 408.7%, on average.

Utz Brands (UTZ – Free Report) engages in the manufacture, marketing and distribution of snack foods in the United States and presently carries a Zacks Rank of 2. UTZ delivered a trailing four-quarter earnings surprise of 8.8%, on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year sales and earnings indicates growth of 1.2% and 10.4%, respectively, from the year-ago numbers.

Sprouts Farmers Market, Inc. (SFM – Free Report) , which is engaged in the retailing of fresh, natural and organic food products, currently carries a Zacks Rank #2. SFM delivered a trailing four-quarter earnings surprise of 15.1%, on average.

The Zacks Consensus Estimate for Sprouts Farmers’ current financial-year sales and earnings implies growth of 11.9% and 24.3%, respectively, from the year-ago numbers.

Financial Market Newsflash

No financial news published today. Check back later.