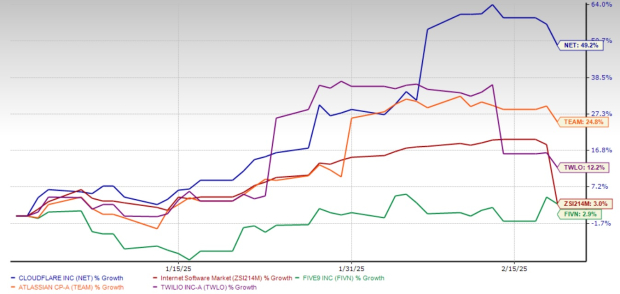

Cloudflare, Inc. (NET – Free Report) has been one of the standout performers in the tech sector, surging 49.2% year to date. The stock has significantly outpaced the Zacks Internet – Software industry, which has risen 3% during the same period. Cloudflare’s rally has also overshadowed its peers, including Five9, Inc. (FIVN – Free Report) , Atlassian Corporation (TEAM – Free Report) and Twilio Inc. (TWLO – Free Report) .

YTD Price Return Performance

Image Source: Zacks Investment Research

Given this impressive run, investors are now left wondering: Should they continue holding Cloudflare or take profits off the table? While valuation concerns and market volatility exist, Cloudflare’s strong fundamentals, expanding enterprise adoption and AI-driven growth initiatives make it a compelling hold for long-term investors.

Cloudflare’s Robust Q4 Results Signal Continued Strength

Earlier in February, Cloudflare delivered another solid quarter, reinforcing its position as a leader in web security, networking and cloud-based services. The company reported fourth-quarter 2024 revenues of $459.9 million, up 27% year over year, beating the Zacks Consensus Estimate by 1.8%. Earnings per share of 19 cents also soared 26.7% and surpassed the consensus mark by 5.6%.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

A key highlight was the 27% year-over-year growth in large customers, with 3,497 enterprise clients now spending more than $100,000 annually on Cloudflare’s services. Revenue contribution from large customers climbed to 69% of total sales, up from 66% in the year-ago quarter, reflecting a growing adoption of Cloudflare’s comprehensive cloud security and networking solutions.

Importantly, Cloudflare’s dollar-based net retention rate improved one percentage point sequentially to 111%, signaling that existing customers are increasing their spending, a crucial indicator of long-term revenue sustainability.

AI and Security-Driven Growth: NET’s Major Competitive Edge

Cloudflare is benefiting from strong demand in cybersecurity, AI-driven automation and enterprise cloud adoption. The company’s Zero Trust security framework, which protects businesses from cyber threats, has gained significant traction. Cloudflare secured a three-year $4 million SASE (Secure Access Service Edge) contract with a major U.S. investment firm during the fourth quarter, strengthening its position in enterprise security.

AI is also becoming a transformative growth catalyst for Cloudflare. The company’s Workers AI and AI Gateway are helping businesses optimize performance and security for AI workloads. Cloudflare’s AI-driven inference capabilities, combined with serverless computing, allow enterprises to scale AI applications efficiently and cost-effectively.

During the last earnings call, management revealed that Cloudflare’s AI offerings provide up to 10 times price-performance improvements for businesses, a clear advantage over traditional hyperscalers. As AI adoption accelerates, Cloudflare’s multi-cloud and edge computing capabilities make it a critical infrastructure player in this evolving landscape.

Cloudflare’s Improved Sales Execution Drives Customer Wins

Cloudflare’s go-to-market execution has improved significantly, thanks to leadership changes and strategic hiring. The company revealed that approximately 80% of new sales representative hires in the fourth quarter were in the enterprise segment, setting the stage for accelerated deal-making in 2025.

Several high-profile customer wins highlight Cloudflare’s growing market presence. A Fortune 100 technology firm signed a five-year $20 million contract, while a leading AI company expanded its Cloudflare partnership with a $13.5 million deal. These deals indicate strong enterprise adoption of Cloudflare’s platform and validate its long-term growth strategy.

Cloudflare’s Profitability and Cash Flow Trend Remain Strong

Cloudflare’s fourth-quarter 2024 operating profit jumped 69% year over year to $67.2 million, with an operating margin of 14.6%, marking a 360 basis-point improvement. Free cash flow for the quarter stood at $47.8 million and $166.9 million for full-year 2024, reflecting Cloudflare’s ability to grow while maintaining financial discipline.

For 2025, Cloudflare is guiding for 25% year-over-year revenue growth, with expected sales of $2.90-$2.94 billion. The company is also increasing its capital expenditure investments in AI infrastructure, positioning itself for sustained long-term expansion. Management anticipates capital expenditure to be 12-13% of total revenues in 2025.

For 2025, management forecasts EPS in the range of 79-80 cents. The consensus mark of 2025 EPS indicates growth of 6.7% and further acceleration in 2026 with an estimated increase of 26.7%. Cloudflare has a strong history of beating earnings estimates. It surpassed the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 20.7%.

Cloudflare, Inc. Price, Consensus and EPS Surprise

Cloudflare, Inc. price-consensus-eps-surprise-chart | Cloudflare, Inc. Quote

Cloudflare’s Premium Valuation: A Key Concern

Although Cloudflare has performed exceptionally and has strong fundamentals, its current valuation raises concerns. While NET has shown impressive growth in customer acquisition and product innovation, such momentum has already been priced into the stock’s valuation, leaving limited room for error.

At present, NET appears overvalued from a price-to-sales perspective. The stock is currently trading at a forward 12-month P/S ratio of 25.41, significantly higher than the industry average of 5.1. This premium valuation raises concerns about the stock’s sustainability, signaling potential downward risk.

Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

Conclusion: Hold Cloudflare Stock for Now

Cloudflare’s 49% YTD rally has been well-earned, supported by robust revenue growth, improving profitability and rising enterprise adoption. While the stock’s high valuation introduces short-term volatility risks, its long-term fundamentals remain compelling.

With continued strength in AI, security and cloud networking, Cloudflare is well-positioned to sustain its momentum. Long-term investors should hold the stock, capitalizing on future upside potential as the company scales its AI-driven solutions and strengthens its enterprise foothold.

Currently, Cloudflare carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Financial Market Newsflash

No financial news published today. Check back later.