Last summer, endpoint security specialist CrowdStrike (CRWD -3.63%) experienced a major hiccup following a widespread outage in its software platform. The days-long blunder resulted in heightened customer panic and frustration, as well as reputational damage to CrowdStrike and its capabilities.

Nevertheless, the company appears to have worked through these challenges, backed up by some resilient operating trends and customer-friendly retention packages. On March 4, CrowdStrike will be reporting earnings for the fourth quarter of its fiscal 2025 (ended Jan. 31). This will mark the company’s third earnings report since the outage occurred.

Below, I’m going to explore how CrowdStrike stock generally performs following an earnings report and make the case for why the stock could be a good buy heading into fourth-quarter results.

How does CrowdStrike stock generally perform following an earnings report?

The chart below illustrates CrowdStrike’s stock price over the last three years. The purple circles with the letter “E” in the middle represent earnings reports.

CRWD data by YCharts

It’s clear that CrowdStrike stock tends to rise following an earnings release. The only notable exception to this trend was in July 2024, when the stock tanked following the release of first-quarter results.

However, the graph shows that these declines were quite pronounced. The reason is that the sell-off was not driven by a lackluster earnings report, but rather the security outage that I alluded to in the intro.

Why I think CrowdStrike stock could continue to soar

While history suggests that CrowdStrike stock should rise following the release of its fourth-quarter earnings, I think investors should keep a keen eye on the following metrics.

First, management is guiding for revenue to be in the range of $1.029 to $1.035 billion, while non-GAAP (adjusted) earnings are forecast to be around $0.86 per share. As part of its retention strategy following the outage, CrowdStrike is allowing for more flexible payment structures as well as less stringent contract terms. As such, investors should keep an eye on how these strategies could impact CrowdStrike’s revenue and profit growth rates.

In addition to meeting or exceeding the guidance above, I think investors should be on the lookout for how well CrowdStrike is cross-selling its applications. A good indicator of this is module adoption rates among CrowdStrike’s customers. According to CrowdStrike’s fiscal third-quarter report, almost 50% of CrowdStrike’s customers were using six or more modules.

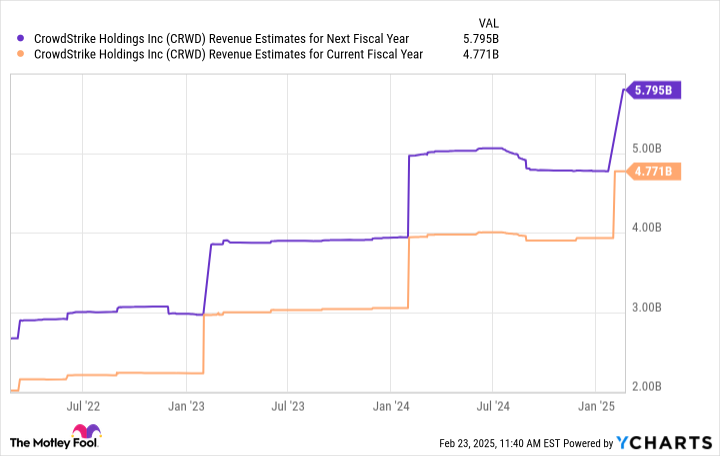

CRWD Revenue Estimates for Next Fiscal Year data by YCharts

To me, Wall Street’s consensus revenue estimates shown above indicate that any turbulence caused by the outage is behind CrowdStrike. Furthermore, investors should not discount the impacts that artificial intelligence (AI) is going to have in the cybersecurity arena. In my eyes, AI is an under-the-radar catalyst for CrowdStrike — and one that could lead to even further module adoption, thereby accelerating revenue growth and widening profit margins.

Image Source: Getty Images.

Is CrowdStrike stock a buy right now?

The one drawback with CrowdStrike is its valuation. The stock has experienced notable valuation expansion over the years, and the chart below indicates that CrowdStrike is much pricier than its peers in the cybersecurity landscape.

CRWD PS Ratio data by YCharts

With that said, CrowdStrike appears to have navigated past the damage caused by the outage and, in the months following, has managed to continue growing revenue and profits. I think the company’s long-term prospects are bright, underscored by the rising need for cybersecurity protocols more broadly, as well as increased investment in AI-powered services.

Despite its lofty valuation, I see CrowdStrike as a compelling buy right now and think the company will impress investors yet again when it publishes earnings in early March.

Financial Market Newsflash

No financial news published today. Check back later.